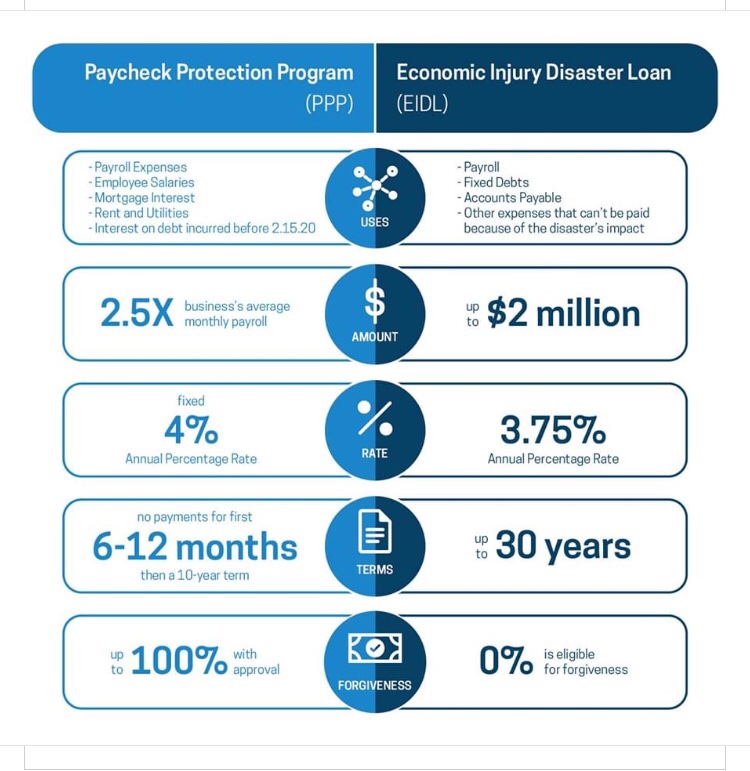

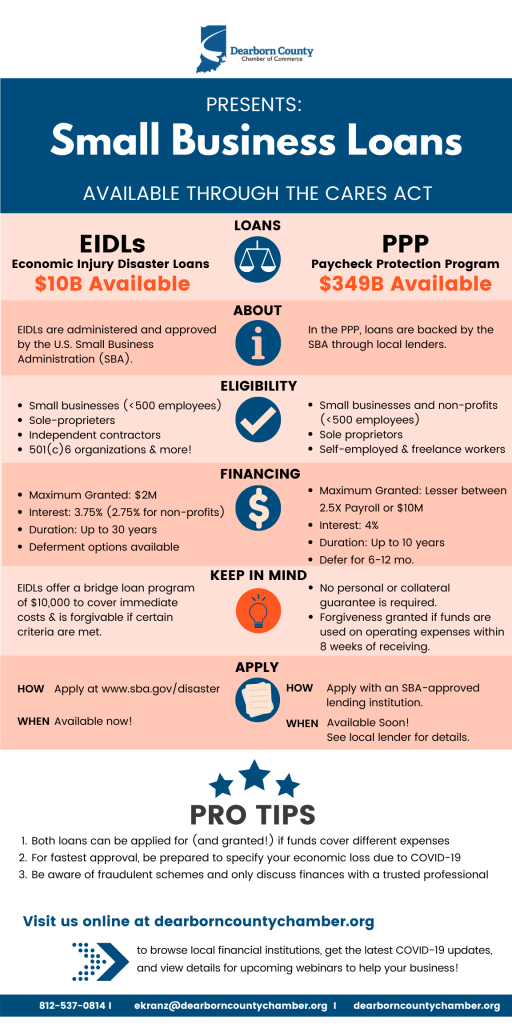

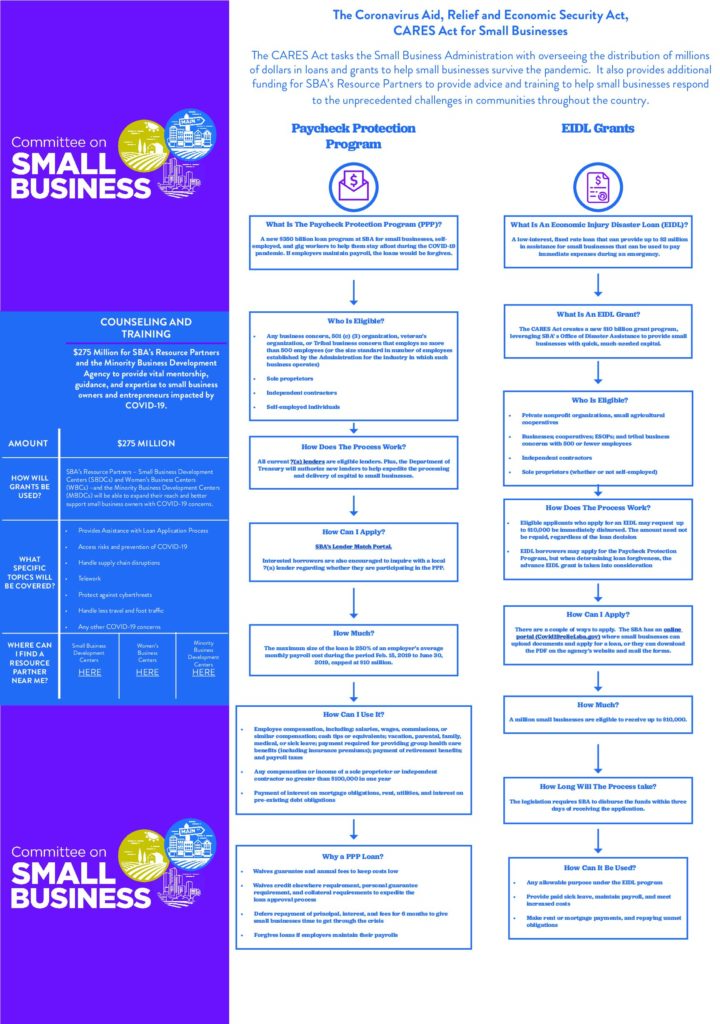

On March 27th, the CARES Act was officially passed, which includes $376 billion in relief available for U.S.-based small businesses impacted by COVID-19.

As we have looked at the CARES Act, we realized that one of the main reasons many small businesses haven’t applied yet is because it’s complicated. There are multiple programs for which a given small business might qualify for, different timelines for each one, and, in many cases, it’s confusing to understand whether your small business is even eligible in the first place. In addition, some lenders have already begun processing loan paperwork, adding a time crunch to an already-stressful process.

With all of that said — we’re here to help. We’ve created some simple recaps for each program, for those small businesses that are needing assistance. And, after speaking with advisors, listening to countless conference calls with banks and accounting firms, and conducting plenty of our own research, we are taking everything we have collected and learned and placing it on this page.

AGAIN WE ARE HERE TO HELP! Feel free to set up a time to speak with someone, getting your books healthy and actionable in order to get assistance, or if you have questions about what route is best for your small business.